As our loved ones age, ensuring they receive the best care becomes a priority. In New Zealand, families often weigh the options between in-home care and retirement village living. Both options have distinct advantages, but understanding their associated costs is crucial for making informed decisions that align with care needs and financial considerations.

Home Care Costs in New Zealand

1. Government-Funded Home Support

For eligible individuals, the New Zealand government provides funding for home care services through the Ministry of Health, district health boards, and ACC (Accident Compensation Corporation). These services are typically assessed based on individual needs and may cover:

- Personal care (bathing, dressing, toileting)

- Household assistance (meal preparation, cleaning, laundry)

- Respite care for family caregivers

Who Qualifies?

To qualify for government-funded home care, a Needs Assessment is required through a NASC (Needs Assessment and Service Coordination) agency. Factors such as mobility issues, medical conditions, and overall independence are evaluated.

Limitations of Government Funding

While this support is helpful, it does not cover all care needs. The number of hours allocated varies significantly, meaning families may need to supplement with private home care.

2. Private Home Care Services

For families needing more flexible, personalised, and extended care, private home care is a valuable option.

Cost Breakdown for Private Home Care in NZ

- Basic Companion Care (e.g., meal prep, light housekeeping): $30–$40 per hour

- Personal Care (e.g., showering, mobility assistance): $40–$60 per hour

- Overnight Care: $250–$400 per night

- 24-Hour Live-In Care: $6,000–$10,000 per month (depending on needs)

The cost varies based on the type of care, number of hours, and qualifications of the caregiver. Some families use a mix of government-funded and private care to balance affordability and support levels.

3. Funding Options for Home Care

While private home care can seem costly, various funding options exist:

- ACC-Funded Care – Covers home care for individuals recovering from injuries

- Work and Income NZ (WINZ) Support – Some seniors may qualify for assistance

- SuperGold Card Benefits – Discounts on specific services

- Health Insurance – Some policies cover home care expenses

Retirement Village Costs in New Zealand

Retirement villages provide seniors with independent living options alongside access to care services if required. The cost structure is different from home care and often includes:

1. Entry Costs: ‘License to Occupy’ Model

Most retirement villages operate on a License to Occupy (LTO) model, meaning residents do not own the unit but have the right to live there. Typical costs:

- Entry Price: $300,000–$1,500,000+ (varies by location and amenities)

- Ongoing Fees: $100–$200 per week (maintenance, rates, communal areas)

2. Additional Fees & Costs

- Deferred Management Fee (DMF): A portion of the unit’s value (20–30%) retained by the village upon exit

- Extra Care Packages: $500–$1,500 per month for assisted living services

- Hospital-Level or Dementia Care: $2,000+ per week

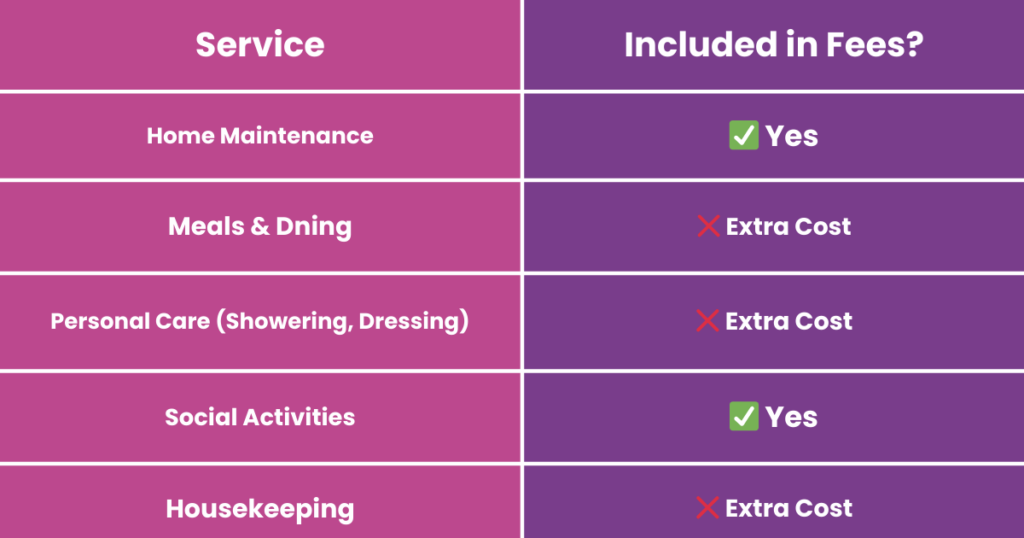

3. What Retirement Villages Cover vs. Extra Charges

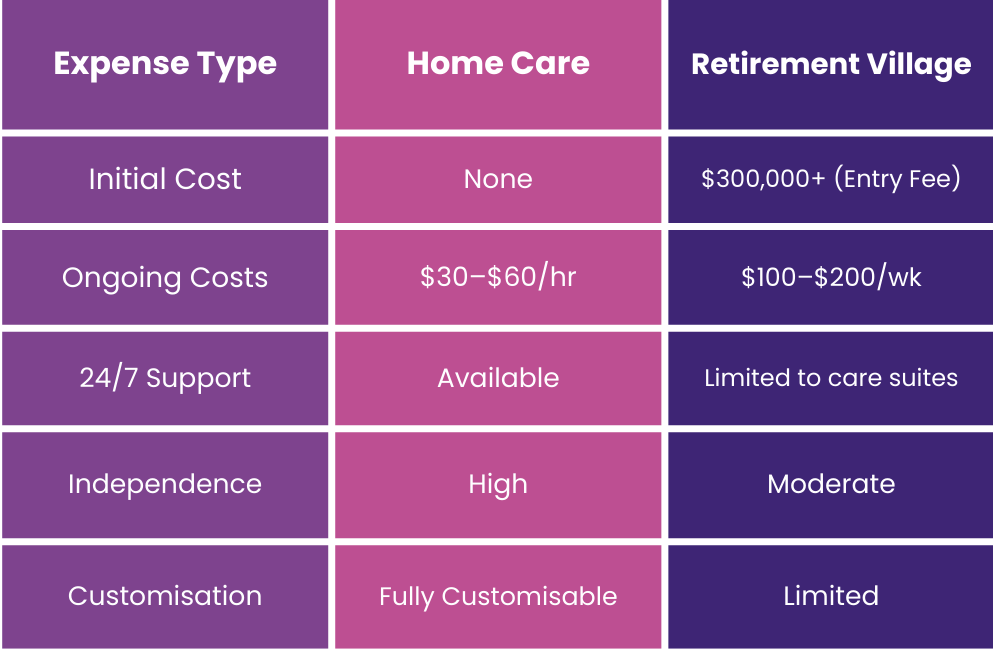

Comparing Home Care vs. Retirement Village Costs

Pros & Cons: Home Care vs. Retirement Villages

Home Care Benefits

Familiar Environment – Seniors stay in their own home, Flexible Care Options – Choose only the services needed, Cost Control – Pay only for required care, rather than full-time fees

Home Care Challenges

- May require home modifications (e.g., ramps, rails)

- If needs increase, costs can rise significantly

Retirement Village Benefits

- Community and social connections

- Access to care services if needed

- Maintenance-free living

Retirement Village Challenges

- High entry cost (non-refundable in most cases)

- Ongoing fees (even if care services aren’t used)

- Limited flexibility in personalisation of care

Financial Planning Tips for Families

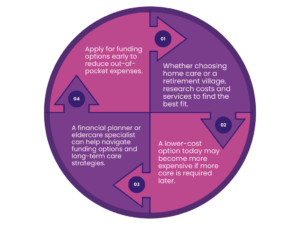

1ï¸âƒ£ Explore Government Subsidies – Apply for funding options early to reduce out-of-pocket expenses.

2ï¸âƒ£ Compare Providers – Whether choosing home care or a retirement village, research costs and services to find the best fit.

3ï¸âƒ£ Plan for Future Needs – A lower-cost option today may become more expensive if more care is required later.

4ï¸âƒ£ Get Professional Advice – A financial planner or eldercare specialist can help navigate funding options and long-term care strategies.

Final Thoughts: Which Option is Best?

The choice between home care and a retirement village depends on individual preferences, medical needs, and financial circumstances. For those who prefer independence and familiar surroundings, home care is often the better choice. However, for seniors who require social interaction and structured support, a retirement village might be a good fit.

âž¡ Want to discuss home care options for your loved one? Call us today for a friendly, no-obligation chat about how we can help.